The COVID-19 pandemic has necessitated unprecedented changes across society and the global economy. It remains to be seen how many of these changes will “stick” in a post-COVID world though certain trends which were already underway, and were able to thrive during the year’s disruptions, will likely see accelerated adoption as a result. The inverse is true for sectors and markets which entered 2020 facing headwinds. For infrastructure investors this has meant a reduction to terminal values for hydrocarbon assets and an increase in the growth outlook for renewable energy (see chart below). The infrastructure of the future, in our view, will be increasingly digital, interconnected, and green. We see 2020 as a key inflection year for renewable energy with accelerated growth to be driven by the following:

- Dramatically falling costs

- Ambitious policy and generous subsidization

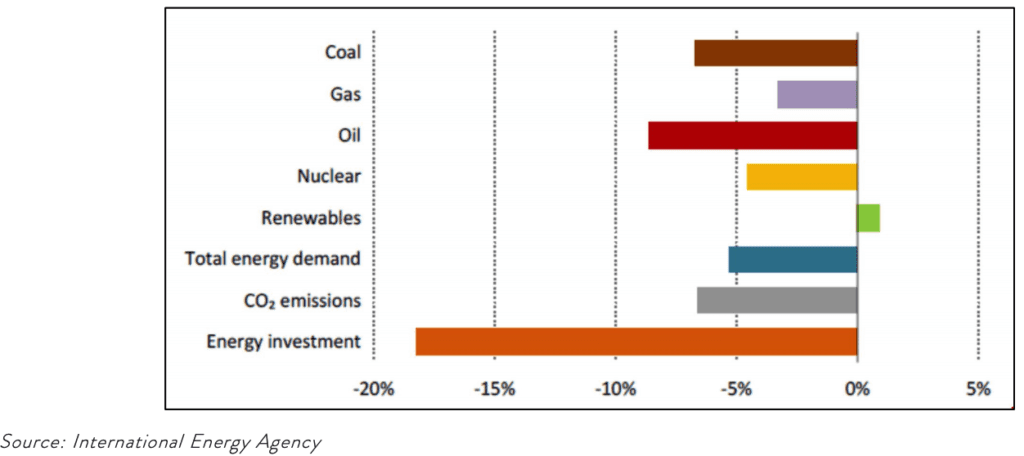

- Capital flows aligning more closely with societal goals (i.e., ESG investing) For example, as shown in Figure 1 below, in 2020 total energy demand fell in every category except renewables.

Figure 1: 2020E Y/Y Change in Energy Demand by Source, Total Emissions and Total Energy Investment

THE ECONOMIC RATIONALE FOR RENEWABLE ADOPTION

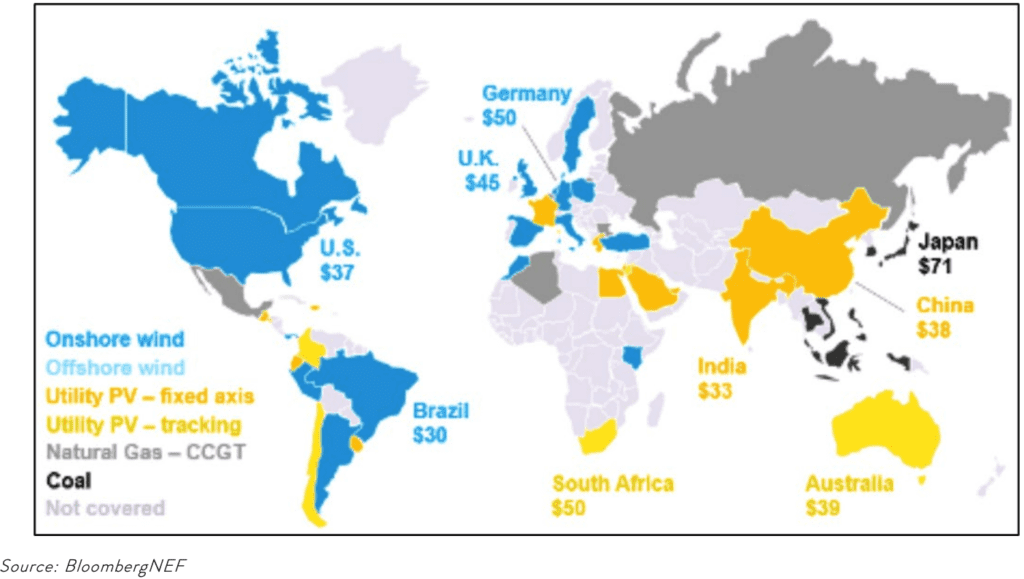

The argument for embracing carbon-neutral energy has begun to shift away from environmental activism towards one grounded in cost competitiveness. Wind and solar are now competitive with coal and natural gas thanks to a combination of technological innovation, market competition and global supply chain integration. As shown in Figure 2 below, renewable energy has become the cheapest option for power generation throughout much of the world.

Figure 2: Cheapest Source of New Bulk Electricity Generation by Levelized Cost of Energy (LCOE) $/Megawatt-Hour (Excludes Subsidies and Tax Credits)

Residential (i.e., rooftop) solar appears especially advantaged in the U.S. as photovoltaic (PV) panel costs have fallen in concert with lithium-ion batteries. While residential solar systems have gotten cheaper, residential utility rates have been relatively flat as rate base growth has offset the decline in generating costs, which has the effect of further increasing solar’s relative attractiveness. Growing storage attachment rates for PV installations has been an important element of solar adoption. Not only does battery storage partially solve the intermittency issues that have long been the solar industry’s Achilles’ heel, but storage also creates dispatching optionality for the asset owner thus increasing overall grid resiliency.

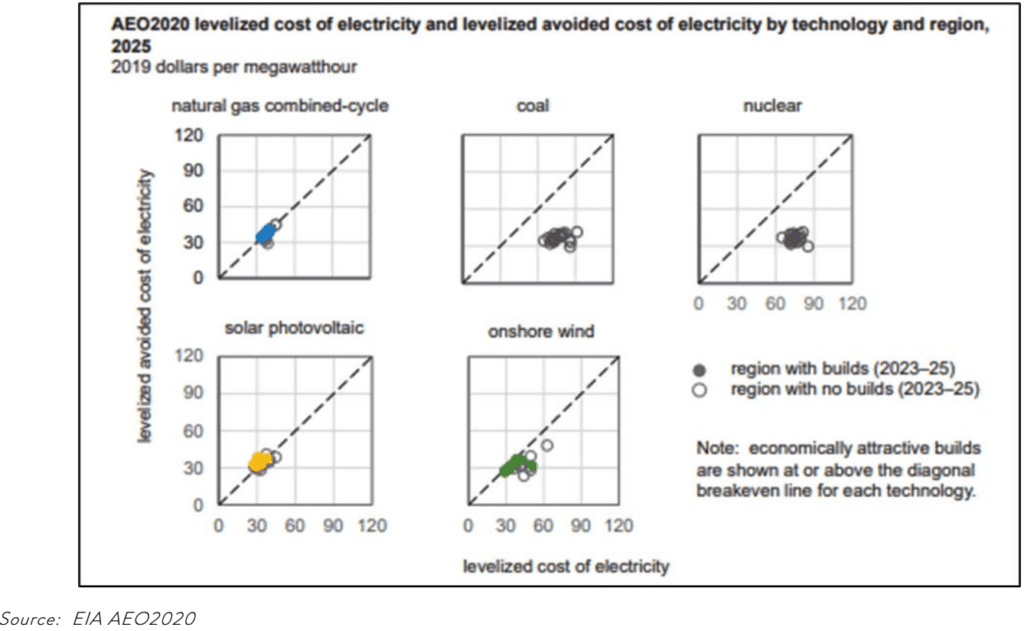

Figure 3: In the US, Solar Photovoltaic (PV) Generation is Economically Competitive with GasFired Combined Cycle Generation.

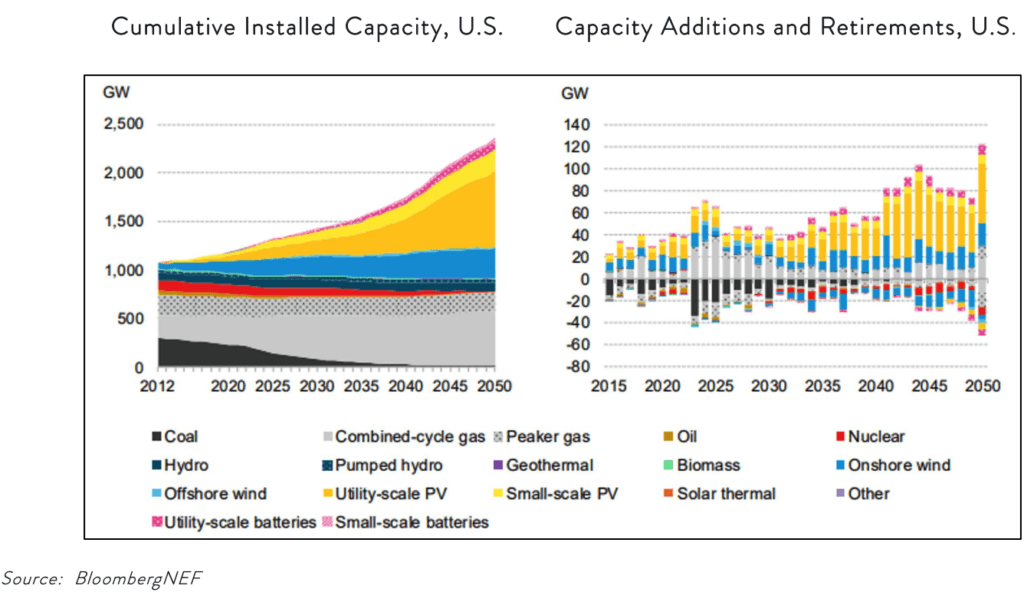

Renewables are also becoming a larger part of the utility-scale generation mix with many regulated utilities currently decommissioning their remaining coal capacity. Several large utilities have even begun divesting natural gas assets such as distribution pipelines with capital being redirected towards onshore and offshore wind, solar, and other renewable generation assets. According to an analysis from BloombergNEF, solar is forecast to grow to ~43% of the US generation mix by 2050 and wind to about 14% as costs continue to decline. The rising penetration is likely to push down the capacity factors of other technologies, increasing the cost of such technologies and leading to a virtuous cycle favoring renewables. As such, while renewable energy is not likely to become 100% of the mix, we believe there is growing likelihood that ~40% of the electricity generation will be comprised of renewables by 2050 with natural gas comprising about a third and the remainder composed of minor amounts of coal, nuclear, oil, and other.

Figure 4A: US Electric Generation Capacity by Source

Figure 4B: US Electric Generation Capacity by Source

Policy incentives, such as the Solar Investment Tax Credit (ITC) in the U.S., will continue to play an important role in renewable adoption. For example, large residential solar installation firms utilize the credit as a source of capital which can be securitized and sold to large investors with sizable tax liabilities providing a cheaper cost of capital than traditional financings. Prior to its extension as part of Congress’ December 2020 COVID-19 relief bill, the credit was slated to taper down in 2021 and 2022 but will now remain at 26% in both years for both residential and nonresidential projects (meaning commercial and utility scale), then step down to 22% in 2023 and 10%/0% for nonresidential/residential in 2024. The tariff of 18% in 2021 on imported modules from China is expected to end by the end of 2021. We expect the Biden administration to push for further extension along with other forms of federal support for renewable energy as part of President Biden’s $2 trillion infrastructure plan.

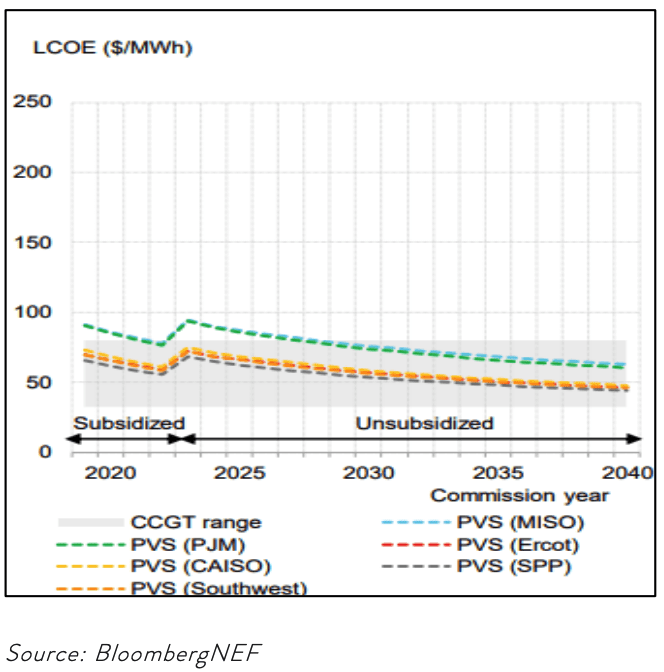

Even without the policy incentives, solar PV plus battery storage is becoming competitive with natural gas fired generation, especially under the assumption that solar only partially replaces combined cycle gas turbines (CCGT). The chart below shows levelized cost of energy (LCOE) with 90% of gas fired generation covered.

Figure 5: Levelized Cost of Energy Solar vs Combined Cycle

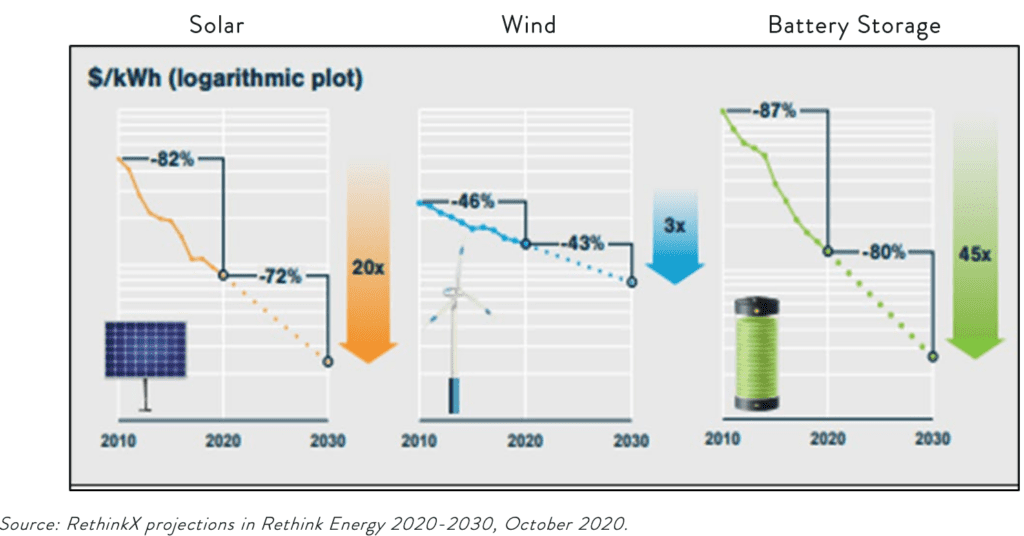

However, the cost of solar is continuing to plummet. According to a study by RethinkX, solar energy costs have fallen by 82% and are expected to fall by another 72% by 2030. This means that solar energy is expected to cost just 5% of what it did in 2010. Battery costs have fallen even further, plunging 87% during the last decade, and are expected to fall another 80% by the end of this decade. Again, this means that battery storage is expected to cost just 2.5% of what it did in 2010 by the end of the current decade.

Figure 6: Renewable energy costs

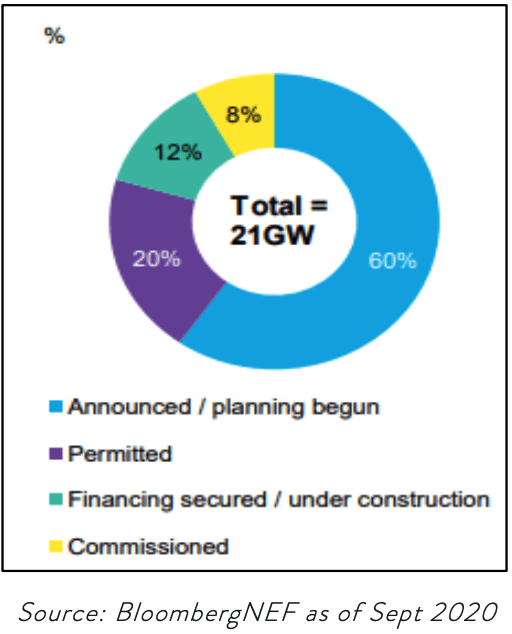

Given the incentives, declining costs, and competitiveness, the US solar plus storage project pipeline is growing. As of the end of 3Q20, there were 21GW of projects.

Figure 7: US Solar Pipeline

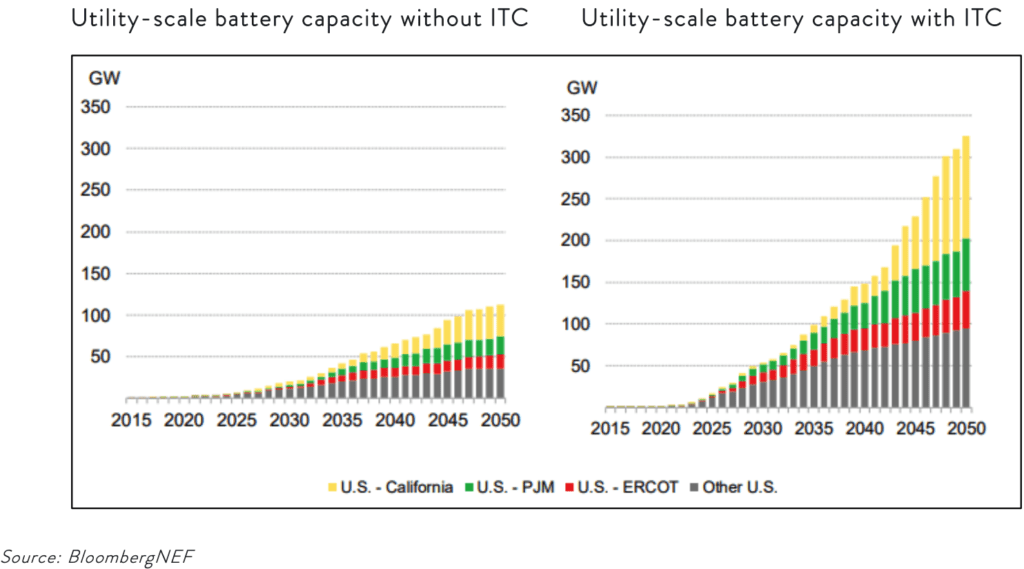

As a result of the expected decline in battery costs, we believe that utility-scale battery capacity is likely to grow rapidly. Utility-scale battery capacity is predicted to grow to 115 GW by 2050. With the ITC utility-scale and renewable portfolio standard mandates battery capacity could reach nearly 3x that amount.

Figure 8: Utility Scale Battery Outlook

Hydrogen is another disruptive green technology which has long been viewed as fringe and noneconomical by experts and analysts, until recently. So called “gray” hydrogen, which is produced using coal and natural gas, has become competitive in certain applications, but nets little improvement in carbon emissions versus natural gas. “Green” hydrogen, on the other hand, is produced via electrolysis from renewable energy sources, but still has a way to go down the cost curve before becoming economically competitive.

Massive investment will be required for green hydrogen to achieve the scale needed to become a fuel alternative for its most natural applications such as long-haul transport, shipping, and industrial production. This requisite investment seems to be on the horizon. The European Union strategy calls for a 650x increase in electrolysis over the next decades from 60 MW currently, to 40 GW by 2030. It is then expected to increase a further 125x, to 500 GW, by 2050 and the European Union has pledged to invest up to 470 billion euros.

Figure 9: European Union Hydrogen Electricity Strategy Calls for Rapid Increase in Capacity

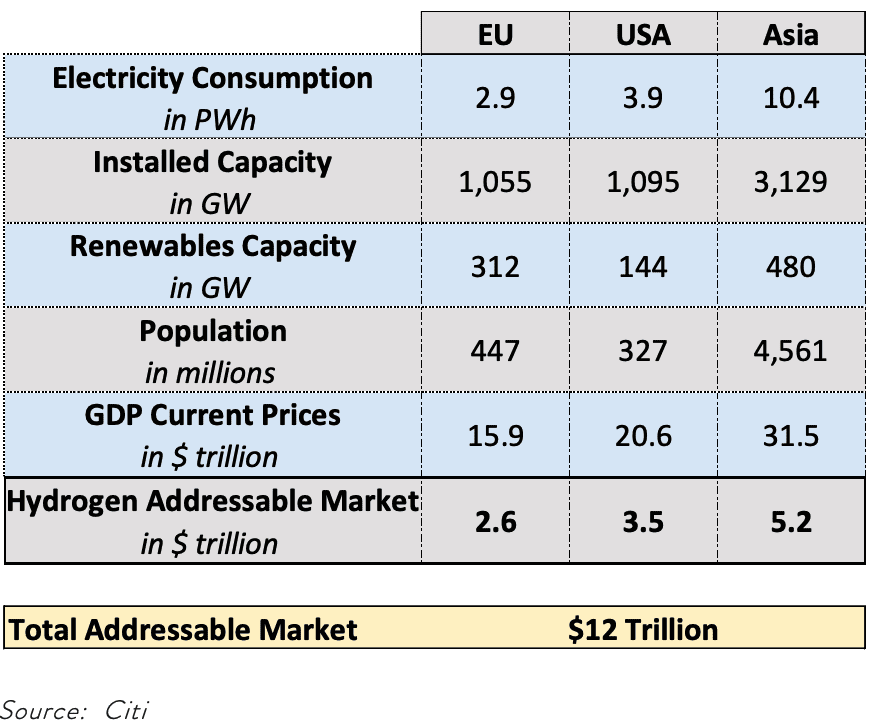

According to Citi equity research, the global addressable market is 10 trillion euros (US$12Trillion) over the next three decades.

Figure 10: The Global Addressable market is potentially $12 Trillion

Any investment of capital, whether public or private, would need to stimulate both the supply and demand side given limited existing infrastructure (the “chicken and egg problem”). Such a “from the ground up” build-out of the hydrogen economy should be undertaken with the goal of creating a virtuous “circular economy” of production, storage, distribution, and retail, per J.P. Morgan research. What is encouraging is the effort to break the chicken and egg problem by Air Products and Chemicals (ticker APD), who has partnered with the Kingdom of Saudi Arabia in a $7 billion joint venture, the largest green hydrogen project of its kind, to fuel 15,000-20,000 truck/buses. There are ~250 mm commercial vehicles in the world which would take 12,000 plants of this size to serve. To serve just 1% of the global bus/truck market would require 125 such plants and an investment of $625B-$875B which helps to define the enormous opportunity presented by hydrogen powered vehicles.

FOSSIL FUELS LIKELY TO REMAIN RELEVANT, BUT PEAK OIL MAY ALREADY HAVE BEEN ACHIEVED

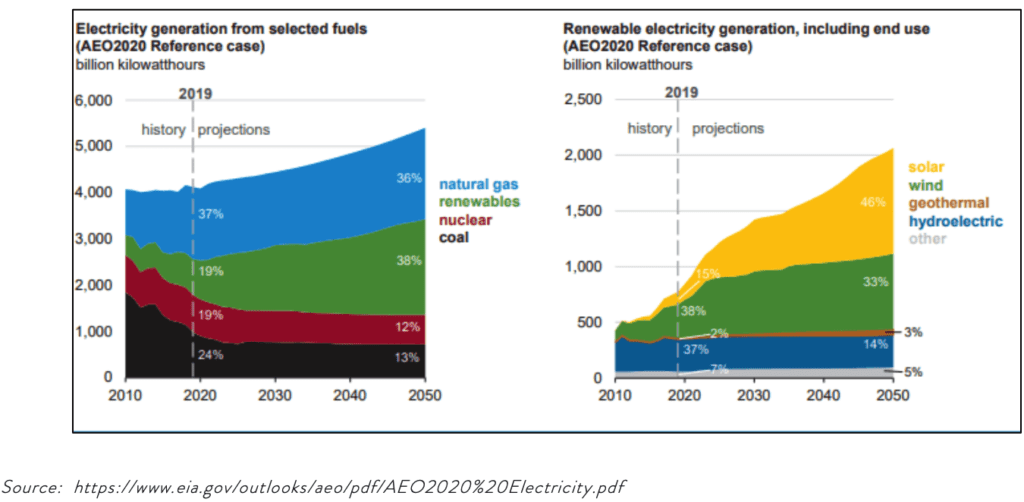

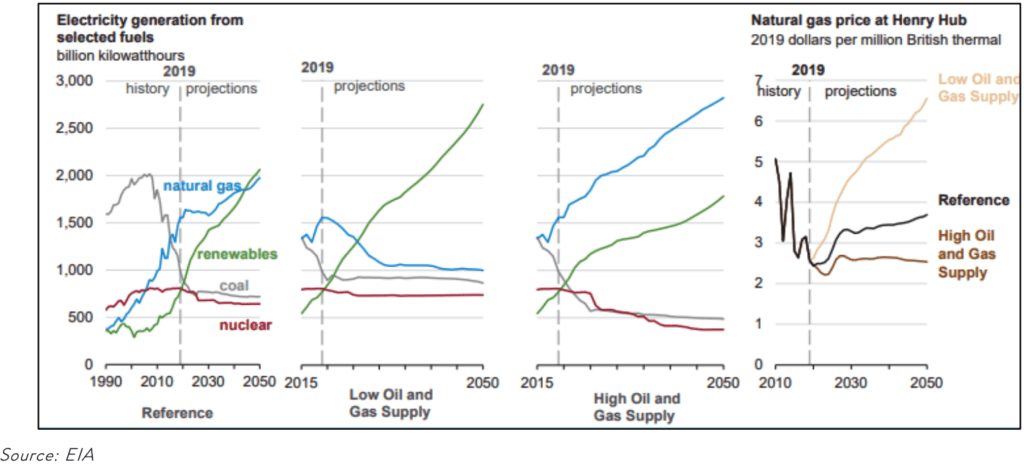

Natural gas remains a cleaner alternative to coal and has the benefit of having robust distribution and power generation infrastructure already in place. Renewable generation will not be capable of powering 100% of the United States’ energy needs for several decades (if ever) and “peaker” natural gas fired power plants will continue to be needed to help stabilize the electric grid. None-the-less, social and policy winds are shifting away from natural gas generation with fewer industry players appearing interested in investing in new capacity for what may end up becoming “stranded” assets.

Figure 11—Electricity Generation from Selected Fuels

We argue that it is rational for capital markets to ascribe premium valuations to assets with less carbon exposure and more heavily discount older technologies for the same reasons. Together with the rise of “ESG” investing, we expect less capital to be freely available for investments in hydrocarbon assets which will further incentivize industry to invest in carbon-neutral projects.

Crude oil demand may see a steeper decline than natural gas as numerous jurisdictions have already set timetables to reduce or eliminate the use of internal combustion engines over the next two decades (e.g. California, China) – a trend that is more likely to speed up than slow down. In addition, a number of vehicle manufacturers have announced plans to phase out internal combustion engines (ICEs) altogether. For example, General Motors has announced plans to discontinue manufacturing vehicles with ICEs in favor of electric vehicles by 2035. Volkswagen said in March 2021 that it expected full-electric vehicles to account for 70% of its European sales by 2030 and 50% of sales in the US and China. They also said they would not develop any new internal combustion engines in the future. Previously it had said it would introduce its last ICE in 2026. This is likely to create incentives like those described above with car manufacturers unlikely to invest in markets where demand decline is a certainty. There is also the risk, from industry’s point of view, of policymakers becoming more stringent in the future or reneging on current targets.

As of November 2020, the IEA forecasts global crude oil demand being down 8.8 mbpd in 2020 versus 2019 (~10% y/y), with a 5.8 mbpd recovery in 2021 (3 mbpd below pre-COVID 2019 demand). Given the trends discussed above, it appears somewhat likely that 2019 could end up being the year of “peak oil” demand.

CONCLUSION

Renewable energy is likely a beneficiary of the political, social, and economic changes seen in 2020. There are numerous ways for investors to participate in the buildout of the world’s burgeoning green infrastructure including traditional publicly traded stocks and yieldco’s, private equity vehicles, fixed income and asset-backed instruments. We believe that there are some attractively priced traditional energy infrastructure investments given the sector’s recent headwinds, but caution investors to take a clearheaded approach to evaluating the long-term outlook for oil and natural gas-based assets.

Click here to download the PDF.

IMPORTANT DISCLOSURE INFORMATION

This commentary is provided for informational purposes only and contains no investment advice or recommendations to buy or sell any specific securities. The statements contained herein are based upon the opinions of the Portfolio Management team and the data available at the time of publication of this report. Any sectors or securities mentioned are based on newsworthiness and may or may not reflect holdings in any Principal Street portfolio. The reader should not infer that any securities discussed were or will be profitable. Information was obtained from third party source s believed to be reliable, are not necessarily all inclusive, and are not guaranteed as to accuracy. Past performance is no guarantee of future results and there is no assurance that any predicted results will actually occur.